How to File Business Activity Statement (BAS) in 2025-26

- Aesha Shah

- November 19, 2025

- 6 minutes

- Blogs

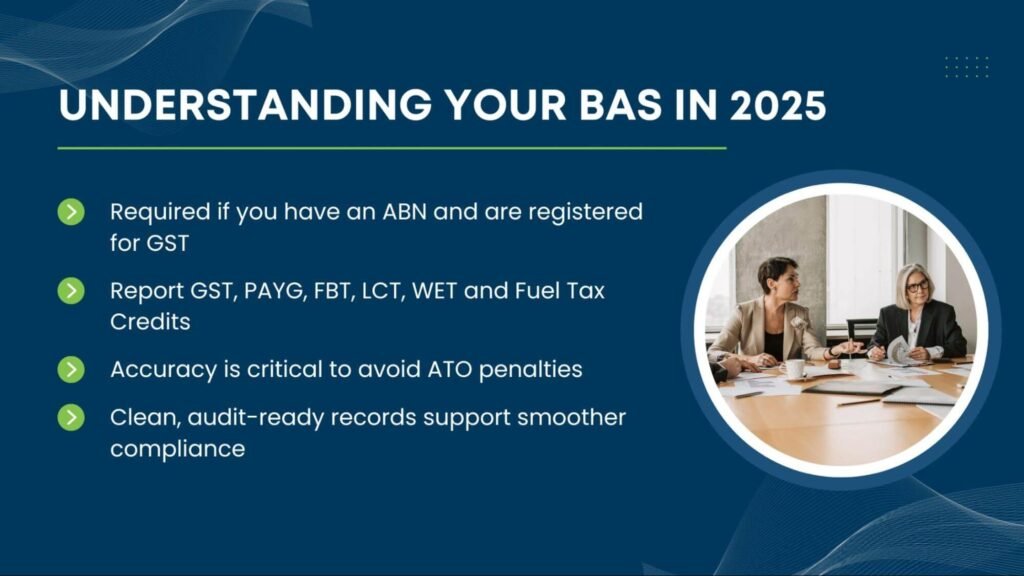

If your organisation has an ABN and is registered for GST, the ATO will automatically issue your Business Activity Statement for each reporting cycle, monthly or quarterly, depending on your requirements. Understanding how to file a business activity statement is essential for nonprofits in 2025, especially with strict accuracy standards and firm lodgement deadlines.

Even small errors can create delays, penalties, or compliance risks, making it crucial to maintain clean financial records and stay audit-ready. Whether your BAS is prepared internally or through an outsourced accounting partner, knowing the requirements supports smoother operations and allows you to focus more on community outcomes.

Key Takeaways

Understanding how to file a Business Activity Statement (BAS) is essential for nonprofits to maintain compliance, avoid penalties, and ensure accurate financial reporting.

Each BAS is customised based on your organisation’s GST status, PAYG obligations, and other tax registrations like FBT, LCT, WET, and Fuel Tax Credits.

Lodgement frequency, annual, quarterly, or monthly, depends on your turnover, making it important to track ATO BAS due dates to avoid missed deadlines.

Working with a registered BAS or tax agent helps reduce errors, improve compliance accuracy, and ensure smooth, stress-free lodgement.

Understanding Your Business Activity Statement: A Complete Compliance Guide

The Business Activity Statement (BAS) is not a generic tax form but a customised reporting tool designed to reflect your organisation’s specific financial activities. Understanding how to file a business activity statement helps you interpret this document clearly, ensuring you meet your obligations with accuracy and confidence.

Your BAS will vary based on your size, structure, and tax registrations, making it essential to know which components apply to your operations and when to lodge business activity statement submissions to stay fully compliant.

Key Components You May Find on Your BAS:

- Goods and Services Tax (GST)

- Pay-As-You-Go (PAYG) Instalments

- PAYG Withholding

- Fringe Benefits Tax (FBT)

- Wine Equalisation Tax (WET)

- Luxury Car Tax (LCT)

- Fuel Tax Credits (FTC)

Goods and Services Tax (GST)

GST is a 10% consumption tax applied to most goods and services sold or consumed in Australia. Organisations that exceed the $75,000 turnover threshold ($150,000 for nonprofits) must register for GST, while others may opt in voluntarily to improve transparency and claim credits. For many nonprofits, annual GST reporting is an option where eligible, simplifying compliance in a low-activity year.

Key GST obligations include:

- Registering once your turnover exceeds the threshold

- Charging 10% GST on taxable sales

- Tracking all GST credits from business purchases

- Keeping accurate GST records

- Reporting GST collected and paid on your BAS

Pay-As-You-Go (PAYG)

PAYG helps organisations spread income tax payments throughout the year. It includes two components: instalments and withholding.

PAYG Instalments

These are periodic prepayments toward your expected annual tax. They:

- Begin after your first profitable tax return

- Offset your year-end tax liability

- Are calculated based on your previous taxable income

PAYG Withholding

If you pay wages, you must register for PAYG withholding. You must:

- Withhold the correct tax from employee salaries

- Report gross wages and withheld tax on your BAS

- Remit those amounts to the ATO

Fringe Benefits Tax (FBT)

Fringe Benefits Tax (FBT) is a separate tax paid by employers on non-cash benefits provided to employees in addition to their salary or wages. If your organisation offers perks such as company cars, entertainment, or expense reimbursements, any FBT payable for the reporting period must be included in your BAS.

Although FBT is calculated independently from GST or income tax, businesses may still need to report instalments or their FBT liability through their BAS, making it essential to track and determine the taxable value of all fringe benefits provided.

Key points to remember about FBT:

- Applies to non-cash benefits provided to employees

- Calculated separately from income tax

- Based on the taxable value of fringe benefits

- Reported as part of your Business Activity Statement

For support in meeting complex compliance requirements across FBT and GST, many nonprofits partner with financial services compliance specialists.

Luxury Car Tax (LCT)

Luxury Car Tax (LCT) is a federal tax applied to the sale or importation of high-value vehicles that exceed the ATO’s annual luxury car threshold.

While it mainly affects car dealers, importers, and individuals purchasing prestige vehicles, any business involved in selling or importing eligible cars must calculate and report LCT through their BAS.

The tax is only applied to the portion of the vehicle’s value that exceeds the set threshold, making accurate valuation and record-keeping essential for compliance.

Key points to know about LCT:

- A 33% tax is applied to the value of a car above the luxury car threshold

- Applies to licensed dealers and individual importers of luxury vehicles

- 2023–24 thresholds: $89,332 for fuel-efficient vehicles and $76,950 for other vehicles

- 2024–25 thresholds: $91,387 for fuel-efficient vehicles and $80,567 for other vehicles

- Calculated only on the amount exceeding the threshold

- Must be reported on the BAS when selling or importing eligible vehicles

Wine Equalisation Tax (WET)

- Applies only to wine manufacturers, wholesalers, and importers

- Tax rate: 29% of the value of the wine

- Calculated and reported through your Business Activity Statement (BAS)

- Requires detailed record-keeping of all wine sales and valuations

Fuel Tax Credits (FTC)

- Available for machinery, heavy vehicles, and off-road business vehicles

- Claimed as a credit on your BAS to offset fuel excise

- Must calculate the eligible fuel used for business activities

- Requires accurate documentation of fuel purchases, usage, and business purposes

How Often Do I Need to Lodge My BAS?

If you’re registered for GST, you must lodge a BAS every reporting cycle, even if you have no activity.

Annual

- For businesses under $75,000 turnover ($150,000 for nonprofits)

Quarterly

- For organisations with a turnover under $20 million

Quarterly Due Dates:

- Q1 (Jul–Sep): 28 October

- Q2 (Oct–Dec): 28 February

- Q3 (Jan–Mar): 28 April

- Q4 (Apr–Jun): 28 July

Monthly

- Required for turnover above $20 million

- Due 21 days after the month-end

(Note: always check current ATO BAS lodgement dates, tax agent guidance if you use a registered agent to ensure agent-specific concessions are applied.)

How to File a Business Activity Statement

You can file your BAS through:

- Your myGov account (sole traders and individuals)

- ATO Online Services for Business

- A registered BAS or tax agent, many organisations choose this route to lodge business activity statement submissions correctly and on time

When lodging yourself, accuracy is essential. You must calculate:

- GST

- PAYG withholding

- PAYG instalments

- Any additional taxes (FBT, FTC, LCT, etc.)

A single miscalculation can trigger ATO penalties.

How to prepare a BAS statement

Before lodging, gather:

- Sales records

- Purchase invoices

- Payroll summaries

- Reconciled bank statements

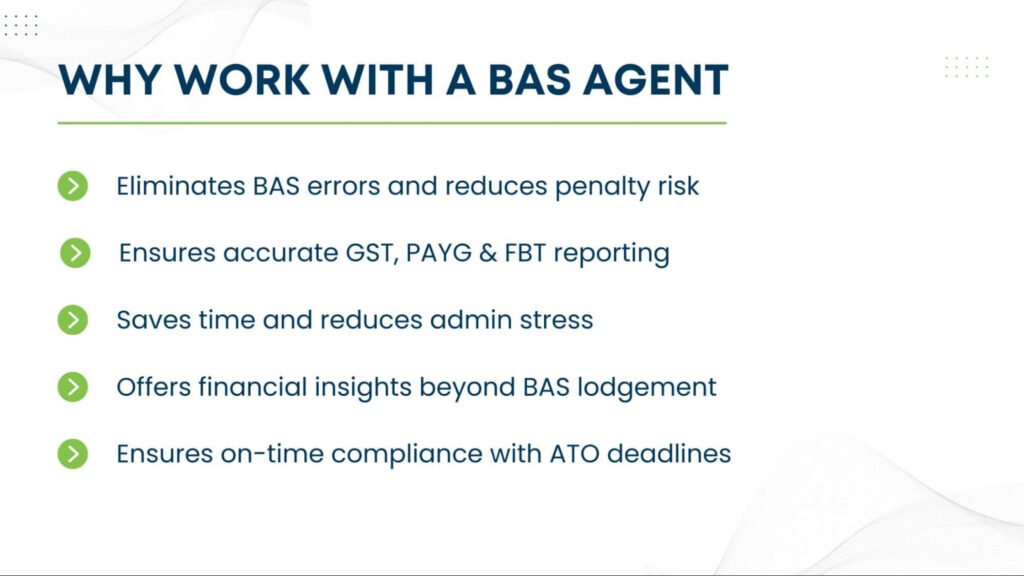

Why Use Professional BAS Support

Many nonprofits choose a registered BAS agent because professionals:

- Detect errors you may miss

- Interpret tax requirements correctly

- Ensure on-time, accurate lodgement

- Reduce penalty risk

- Free your organisation’s time

- Provide additional financial insights

Why ATO BAS Due Dates Matter for Your Business

Understanding your ATO BAS due dates is more than just ticking a compliance box, it’s essential for avoiding penalties, maintaining cash-flow stability, and ensuring your records remain accurate throughout the year.

When you prepare BAS statements correctly and ahead of time, you give your business the financial visibility it needs to plan tax payments and manage expenses.

Many businesses work with an ATO BAS lodgement dates tax agent to avoid confusion around quarterly and annual deadlines, especially when juggling payroll, GST, PAYG, and other tax obligations.

Conclusion

Lodging your BAS doesn’t have to be overwhelming. With the right preparation and clear understanding of your obligations, you can manage your Business Activity Statement with confidence and avoid unnecessary stress.

And if you ever find the process too complex, working with a professional can make BAS lodgement smoother, more accurate, and fully aligned with your responsibilities.

Whether you choose to lodge yourself or rely on expert support, staying proactive ensures your business remains compliant and on track with its financial goals, especially when keeping up with changing ATO BAS due dates.