Converting MYOB to Xero has become a strategic move for many Australian businesses aiming to enhance flexibility, automate processes, and gain real-time financial visibility. As digital accounting continues to evolve, more organisations are choosing to change from MYOB to Xero to simplify workflows and make data-driven decisions with confidence.

This guide unpacks why so many firms are transitioning, highlights the advantages Xero offers over traditional systems, and outlines the essential steps to ensure a smooth migration. Whether you’re still exploring options or ready to leap, in this article, NCS Australia provides practical insights to help you navigate the process and understand how it can transform your business operations.

MYOB vs Xero: A Quick Overview

When you compare Xero and MYOB, both provide robust accounting features, but their approaches differ. MYOB, developed in Australia, is trusted for its comprehensive financial tools and offline functionality for small and medium-sized businesses.

On the other hand, Xero, a cloud-based platform from New Zealand, is widely recognised for its intuitive interface, automation, and real-time reporting. Many businesses now evaluate this MYOB Xero comparison to see which system best supports growth, collaboration, and efficiency.

Before you convert MYOB to Xero, consider these key factors to ensure a successful migration:

- Data Compatibility: Assess which historical data, transactions, and reports can be accurately migrated to Xero.

- Integration Requirements: Identify the third-party apps and bank feeds currently used in MYOB and confirm their compatibility with Xero.

- User Training: Ensure your team receives adequate training to understand Xero’s dashboard, reporting tools, and automation features.

- Compliance and Accuracy: Verify that financial data aligns with Australian accounting and tax regulations post-migration.

- Migration Partner: Choose a reliable migration tool or partner, such as Jet Convert MYOB to Xero, to streamline the process and minimise errors.

What Australian Businesses Must Consider Before Migrating from MYOB to Xero

Before you convert MYOB to Xero, consider more than just the technical migration. The decision should factor in costs, features, integrations, and long-term usability to ensure your financial systems boost efficiency, visibility, and team productivity.

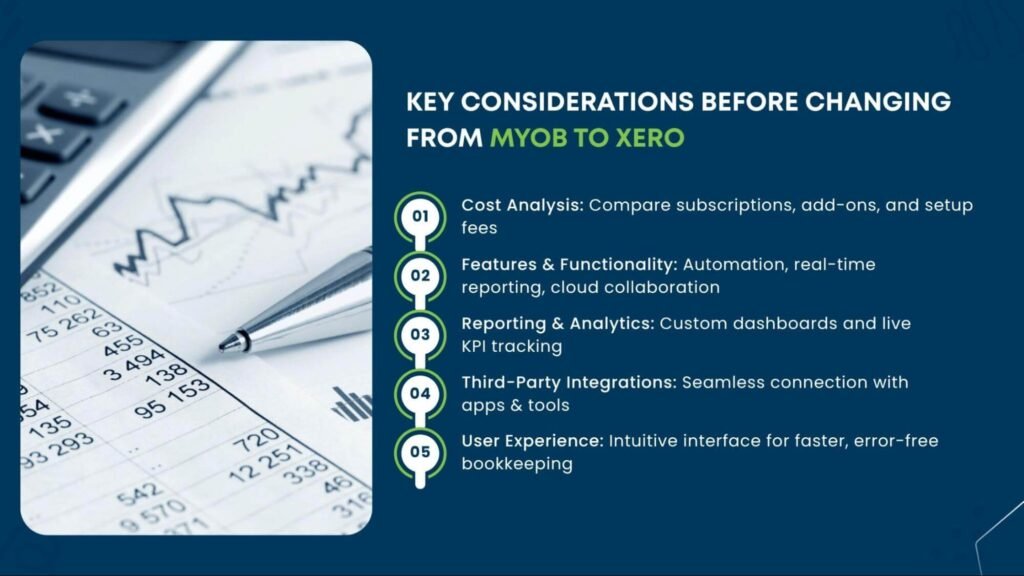

Here are the key considerations Australian businesses should evaluate before making the switch:

- Cost Analysis: Review the pricing of both platforms, including subscriptions, add-ons, and setup costs. Xero’s 2025 small business plans range from AUD $33 to $85 per month, while MYOB often adds fees for payroll or advanced features. Consider whether Xero’s automation and efficiency gains justify the investment.

- Features and Functionality: When comparing MYOB vs Xero, consider which best supports your operations. Xero offers automation, real-time bank feeds, and cloud collaboration, while MYOB is strong for offline access and legacy workflows. Understanding your team’s priorities ensures a smoother transition.

- Reporting and Analytics: Strong financial decision-making relies on effective reporting. Compare both systems’ analytics to see how easily you can generate insights, track performance, and create custom dashboards. Xero’s live KPI tracking helps streamline strategic planning.

- Integration with Third-Party Apps: Modern businesses need connected systems. Check if Xero integrates with your CRM, inventory, or payment platforms. With 1,000+ app integrations, it’s highly flexible for Australian SMEs.

- User Experience: Assess how intuitive each platform is. A well-designed interface speeds up bookkeeping and reduces errors. Xero’s cloud-native design is praised for simplicity and ease of use, ideal for digital-first teams.

By assessing these critical areas, your organisation can make an informed decision that ensures not just a migration, but a long-term transformation in how your business manages finances and growth.

6 Simple Steps to Migrate from MYOB to Xero

Migrating from MYOB to Xero doesn’t have to be daunting. With proper planning, the right tools, and a clear process, your business can transition smoothly while ensuring accuracy and compliance.

A structured, step-by-step approach, from preparation to final reconciliation, is key to a successful migration. Here’s how to confidently convert MYOB to Xero in six simple steps.

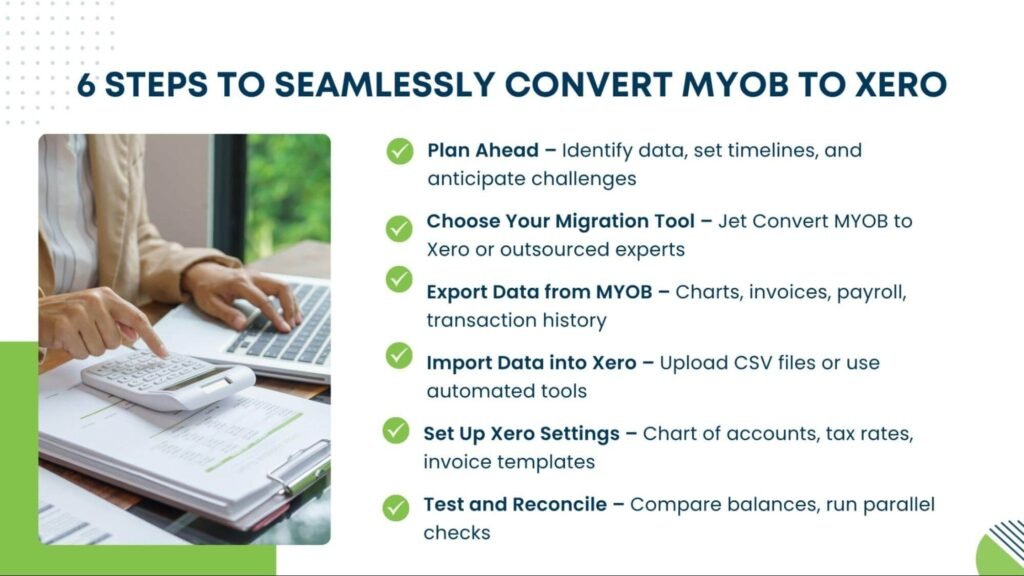

1. Plan Ahead

Invest time in preparation. Identify the data to migrate contacts, invoices, payroll, and historical transactions and set a clear timeline. Planning early helps anticipate challenges and ensures a smooth transition without disrupting workflows.

2. Choose Your Migration Tool

Select the right tool for a seamless migration. Many businesses use Jet Convert MYOB to Xero, officially recommended by Xero, to automate data transfer. Alternatively, professional outsourced accounting providers can manage the process securely and accurately.

3. Export Data from MYOB

Export your chart of accounts, invoices, bills, payroll, and transaction history. This can be done via MYOB’s export function or by outsourcing experts to ensure completeness and accuracy.

4. Import Data into Xero

Upload your exported data into Xero, typically via CSV. Tools like Jet Convert can automate this step and reduce errors, ensuring your financials align with reporting dates for a clean start.

5. Set Up Xero Settings

Configure Xero to match your business operations, chart of accounts, tax rates, payment terms, user permissions, and invoice templates. Customisation ensures consistency while leveraging Xero’s automation and cloud flexibility.

6. Test and Reconcile

Review financial data, compare trial balances, and reconcile accounts. Running both systems in parallel briefly can catch discrepancies early, ensuring accuracy before fully operating in Xero.

A structured approach not only ensures a successful migration but also boosts long-term efficiency. According to Xero’s 2024 Small Business Insights, businesses that digitise and automate accounting save up to 10 hours per week on manual bookkeeping.

Helpful Tips for a Smooth Transition from MYOB to Xero

Successfully converting MYOB to Xero requires careful preparation and a thoughtful approach. By following best practices, businesses can minimise disruptions and make the transition as seamless as possible. Here are some key tips to ensure a smooth migration:

- Gather Essential Data: Collect all relevant information, including employee and customer records, invoices, bank statements, and historical transactions, before starting the migration. Having complete and organised data will make the import process into Xero far more efficient.

- Familiarise Yourself with Xero: Take time to explore Xero’s interface and features. Understanding how dashboards, reporting tools, and automation functions work will help your team navigate the system confidently once the data is migrated.

- Start Small: Begin by transferring a limited set of data, such as a few months’ worth of transactions. This approach allows you to test the process, identify any errors, and make corrections without risking large volumes of information.

- Exercise Patience: Adapting to a new accounting platform can feel challenging initially. Move methodically, provide training for your team, and allow a learning period to ensure a successful transition from MYOB to Xero.

By applying these strategies, businesses can achieve a smoother migration, minimise errors, and fully leverage Xero’s cloud-based capabilities for real-time financial insights.

Conclusion

Transitioning from MYOB to Xero is more than just moving data, it’s an opportunity for Australian businesses to enhance efficiency, automate workflows, and gain real-time financial insights. Careful planning, selecting the right migration tools such as Jet Convert MYOB to Xero, and following a structured approach ensure a smooth and accurate transition.

When you compare Xero and MYOB, Xero’s cloud-based platform, intuitive interface, and extensive integrations clearly stand out, making it an ideal choice for businesses seeking scalability and streamlined accounting processes.

Understanding this MYOB Xero comparison allows organisations like NCS Australia to make informed decisions and confidently embrace the advantages of modern, digital accounting.